Key Takeaway

Branch offers superior value with a debit card that includes full banking services and no monthly fees. rapid! only has basic paycard functionality with additional costs. In our analysis, Branch provides better financial inclusion and lower total costs for businesses and employees.

Quick Navigation

- Platform Comparison Overview

- Key Differences

- Debit Card vs Traditional Paycard

- Pre-funding Requirements

- Fee Structure Comparison

- Platform Similarities

- Frequently Asked Questions

Key Terms

If you're looking for a pay card for employees, you may notice that there are many choices available. One option is the rapid! pay card issued by Green Dot Bank.

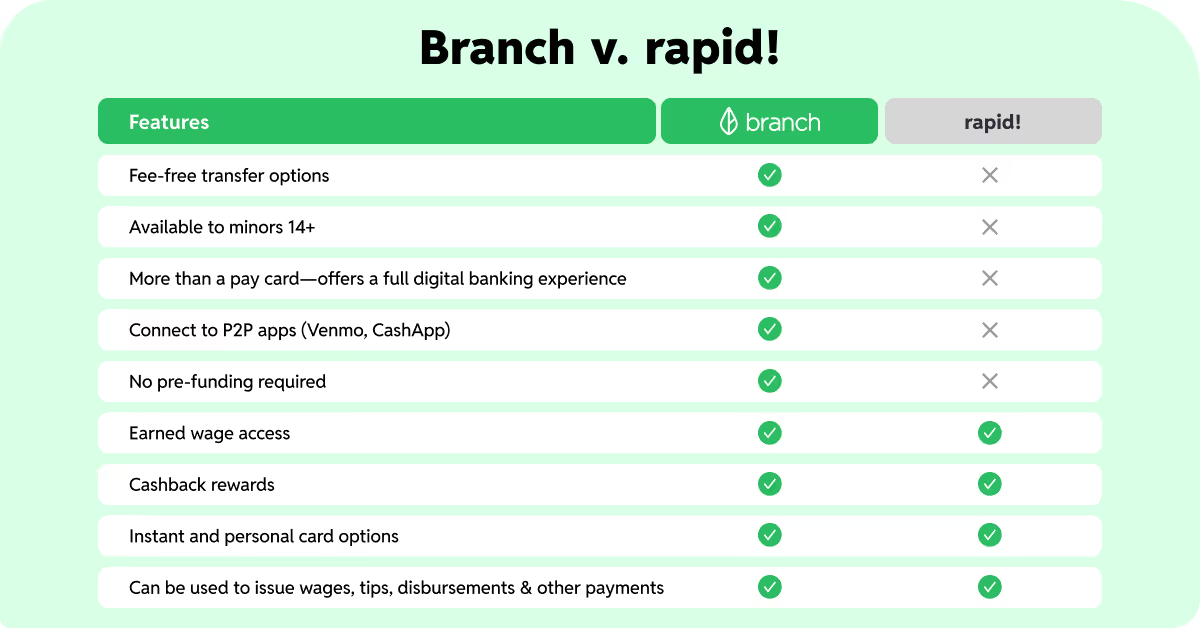

Both Branch and rapid! offer a fast, digital pay solution for employees, but there are key differences between our solutions. Most notably, the Branch Card is a debit card for employees, while rapid! is a traditional pay card.

What Are the Key Differences Between Branch and rapid!?

What Are the 3 Main Differences Between Branch and rapid!?

Here are the most important distinctions to consider when trying to decide between Branch and rapid!

1. Debit Card vs. Traditional Paycard

Branch offers a debit card for employees, while rapid! offers a pay card for employees. Why does it matter?

Branch Debit Card

Branch is a debit card for employees that can be used to pay workers. It comes with a digital banking experience to support more of your workforce, including unbanked workers, workers with limited documentation, and minors 14+.

Benefits:

- Full digital banking experience

- Banking history creation for loans/mortgages

- Supports unbanked workers

- Comprehensive financial services

rapid! Traditional Paycard

A pay card, also known as a payroll card, is similar to a debit card, but has one key difference: it's not linked to a bank account. Instead, a pay card uses a separate account, usually provided by a third party, to hold prepaid wages.

Limitations:

- No banking services

- Limited financial history building

- Basic prepaid functionality only

- May exclude unbanked workers from broader financial services

Banking History Impact: A banking history is often needed to get loans, mortgages, or other financial services. Branch helps workers build this crucial financial foundation.

2. Pre-Funding for Disbursements

Essentially, pre-funding requires companies to tie up capital in a separate account to fund advances.

Branch No Pre-funding

Not Required:

- We front money for worker payments

- No capital tied up

- Simplified cash flow management

- Reduced administrative burden

rapid! Pre-Funding

Required:

- Must maintain pre-funded account

- Ties up business capital

- Complex cash flow management

- Additional administrative overhead

3. Fee Structure

Offering a new financial service to your workers is great, but if it has excessive fees, it may do more harm than good.

Branch Fee Structure

Fee-Free Benefits:

- No monthly maintenance fees

- 8 free in-network ATM transactions per month

- No transaction fees for EWA advances

- Free fund deposits to Branch account

rapid! Fee Structure

Multiple Fees:

- Monthly maintenance fees

- ATM fees

- $1.00 per EWA transaction (max $6/month)

- Various transaction fees

Branch users can always receive funds to their Branch account for free, where they can save or spend their money as they wish.

What Are the Similarities Between Branch and rapid!?

Despite their differences, both platforms offer several common features that make them good paycard solutions.

1. Earned Wage Access

Both Branch and rapid! offer earned wage access options. Earned wage access is a feature that lets your employees request an advance of a part of their wages before payday. They can use it to cover emergency expenses or for other unexpected needs.

Cost Difference: While Branch allows your employees to take advances fee-free, rapid! charges $1.00 per transaction with a cap of $6.00 per month.

This is not a required feature, but many businesses like to offer EWA because it's an in-demand benefit that employees want. Just make sure that the EWA you pick doesn't have hidden fees for you or your workforce.

2. Cashback Rewards

It's always smart to choose a pay card that provides additional financial wellness perks to your workforce. Both the Branch Card and rapid! pay card offer cashback rewards on everyday purchases.

Branch Additional Features: Branch also has a savings goal feature, personalized spending insights, and financial literacy content. Workers can access Greenhouse, a curated marketplace for additional financial products, powered by MoneyLion.

3. Different Payment Types Allowed

Both the Branch Card and rapid! pay card allow companies to issue wages, tips/mileage reimbursements, and other types of payments to worker's cards. This provides flexibility for one-off payments, such as stipends, bonuses, and even last-day pay or final paychecks.

Both cards also have instant or personalized options that allow you to start paying more people on Day 1, while providing the flexibility of a personalized upgrade down the line.

Frequently Asked Questions About Paycard Options

What's the difference between a debit card and a traditional paycard?

A debit card is linked to a bank account with full banking services, while a traditional paycard uses a separate prepaid account without banking features like savings or financial services.

Which paycard has lower fees — Branch or rapid!?

Branch has lower fees with no monthly maintenance fees, no transaction fees for advances, and 8 free ATM transactions per month. rapid! charges monthly fees and $1 per EWA transaction.

Do both Branch and rapid! require pre-funding?

No, Branch does not require pre-funding and fronts money for payments. rapid! requires companies to tie up capital in a pre-funded account for instant disbursements.

Which paycard is better for unbanked employees?

Branch is better for unbanked employees because it provides full digital banking services, including savings accounts and financial history building. rapid! only offers basic paycard functionality.

How to Find the Best Pay Card for Employees

Whether you go with a debit card that comes with free digital banking like Branch or a pay card like rapid!, it's important to determine what your business and workforce needs from a payments solution in the first place.

Carefully weigh your options to determine what makes sense for your business and the people who power it. In our experience working with employers, we've found that comprehensive solutions with lower fees and full banking services provide the best long-term value for both companies and employees.

Unlock a Happier, More Productive Workforce